In recent years, home values have risen significantly, letting homeowners in Kentucky build equity quickly. These days, just about everyone is feeling the effects of inflation, and with costs for everything from groceries to home fixes on the rise, more and more people are eyeing that equity in their homes. It can be smart cash for significant needs like fixing up your house, college tuition, or paying down old debts. In this guide, we will discuss two popular options - home equity loans and HELOCs. Here's how to know the difference and decide what works best for you.

What Is a Home Equity Loan?

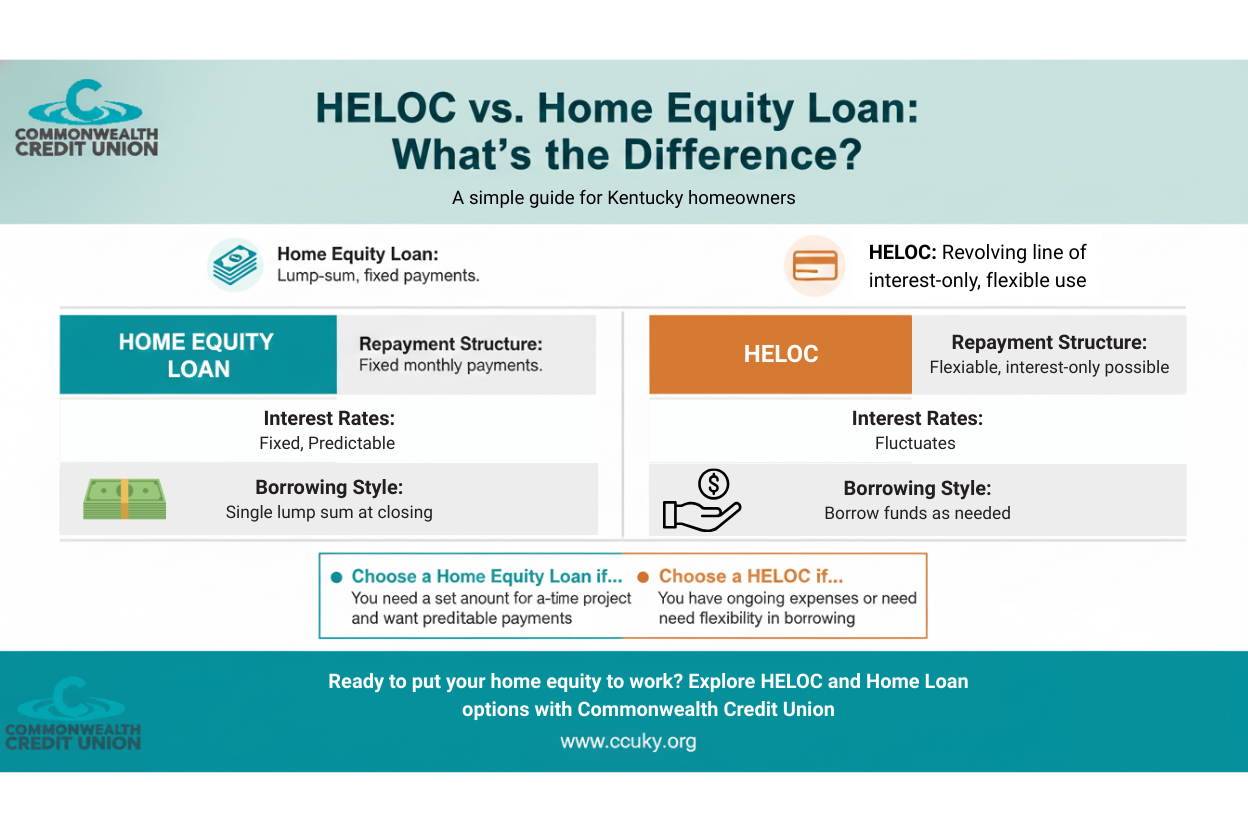

Simply put, a home equity loan is a lump-sum loan based on your home equity, acting like a second mortgage on your property. Borrowers receive a fixed interest rate and predictable monthly payments that don't change. The loan is secured by your house, so payments go toward principal and interest from the start. These features make home equity loans a great choice for one-time large expenses. At Commonwealth Credit Union, we are proud to be local lenders who offer our customers competitive rates and personal support.

What Is a HELOC?

A home equity line of credit, or HELOC, is a revolving line of credit that you borrow from the value of your home. It comes with variable rates, flexibility to draw and repay multiple times, and interest only on what you use. So, suppose you get approved for a $20,000 line of credit, but only use $15,000. You'll pay the interest on the smaller amount. Many people find a HELOC to be a favorable choice for expenses such as ongoing projects, college tuition over several years, or emergency funds. Commonwealth Credit Union offers Kentucky-based HELOCs with flexible terms.

.png)

Home Equity Loan vs. HELOC

So, when the time comes, which should you choose? It is important to know the key differences between a home equity loan and a HELOC, and consider the pros and cons of each one.

- Interest Rate Structure: Fixed vs. Variable Explained

Home equity loans lock in a fixed rate, regardless of market fluctuations. By contrast, HELOCs start with variable rates; however, they can climb significantly if rates rise. In a steady economy, fixed rates give more peace of mind. But if rates drop, a variable rate can save cash, but it is important to remember that there are no guarantees.

- Access to Funds: Lump Sum vs. Draw Period Flexibility

With a home equity loan, you get the entire amount at closing, leaving you with a lump sum of cash. A HELOC, however, spreads it out. For example, you can borrow $10,000 for tuition, then $15,000 down the road for home improvement. Lump sum loans may be best for borrowers with one-time needs or expenses, while a HELOC might be best for long-term or ongoing needs.

- Repayment Schedules and Payment Flexibility

Home equity loans start full payments immediately - principal plus interest over a certain period of years. HELOCs begin with interest-only during draws, then full payback later.

Which Option Is Right for You?

A Home equity loan is typically the best option for predictable, one-time large expenses, while a HELOC may be the best choice if you want flexibility and ongoing access to funds. Commonwealth Credit Union is a Kentucky-based credit union where we work with members to find the right solution.

Apply Online For a HELOC or Home Equity Loan

Ready to put your home's equity to work? Explore our flexible HELOC and home equity loan options today with Commonwealth Credit Union.

Image Source: nampix / Shutterstock