Key Takeaways / Summary:

-

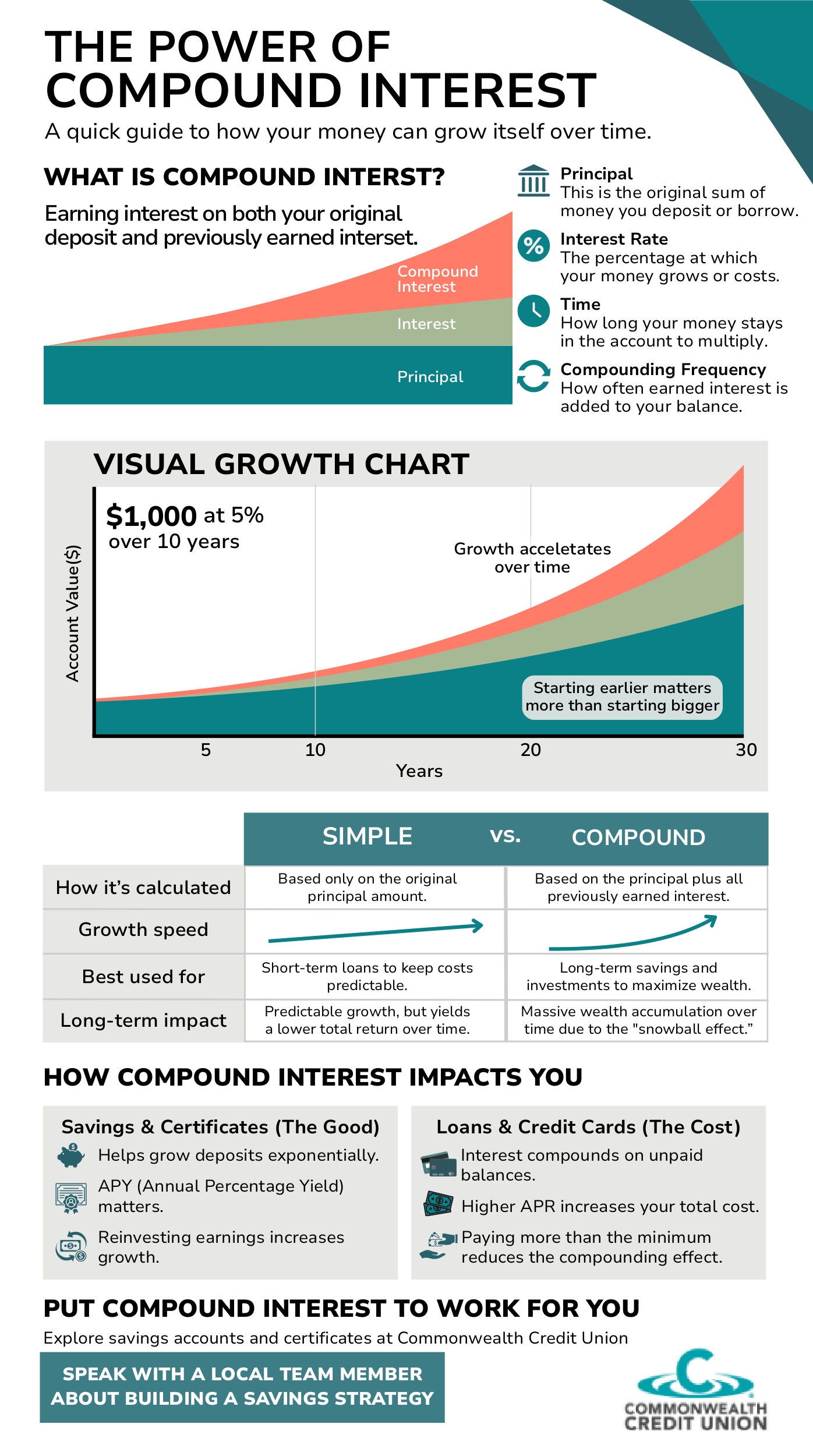

Compound interest accumulates on both principal and interest.

-

The speed of balance growth is determined by factors such as interest rates, the length of time money is invested or borrowed, and the frequency of compounding.

-

Compound interest helps your savings grow faster, but it also makes your loan balances grow faster.

Whether you have a savings account or a loan, the bank or lender calculates interest both on the principal that you initially saved or borrowed and any interest that accumulates. This means your savings will grow faster than you might expect, but so will your loan balance. Understanding the definition of compound interest, how it's calculated, and how it works in real situations can help you make the right financial choices for your life. Commonwealth Credit Union supports our members with savings and loan options.

What Is Compound Interest?

Compound interest is the interest that accumulates on both the initial deposit or loan amount and interest on those funds. With simple interest, on the other hand, interest would only be calculated on the initial principal. To calculate compound interest, you'll need to know the compounding period, or how often the interest is added to the total principal.

Think of compound interest like a snowball rolling down a hill; the bigger it gets, the more snow it picks up, and the faster it grows.

The easiest way to see how compound interest works is with an example. If you put $1,000 in a savings account at 5% compounded monthly, you would have $1,051.16 after the first year and $1,104.94 after the second year. With simple interest, you would always earn $50 per year, leaving you with $1,050 after the first year and $1,100 after the second.

_page-0001.jpg)

The Compound Interest Formula

To determine compound interest, subtract the principal from the result of the principal multiplied by (1+ interest rate/compounding frequency), raised to the power of (compounding frequency multiplied by time).

The principal is the initial deposit or loan balance, and the interest rate is the annual rate. Instead of only earning interest on your original amount (the principal), you also earn interest on the interest that has already been added to your account. The more often this happens, the faster your balance increases. While the specific math involves powers and compounding frequencies, the most important factor is time: the longer you leave your money alone, the more exponential growth you will see. The more often interest compounds, the faster the account grows. However, time is the biggest factor.

Compound Interest and Savings Growth

The combined power of time and compound interest helps you save for the future. As discussed in an earlier example, a contribution of $1,000 in a savings account at 5% interest compounded monthly results in a balance of $1,051.16 after the first year. If you left that money in the account for 10 years, the balance would become $1647.01, and after 40 years, $7358.42. This is a type of exponential growth, where the rate of growth speeds up over time.

Contributing to retirement accounts and long-term savings as early as possible lets you truly take advantage of compound interest.

Compound Interest on Loans

When it comes to loans, unpaid credit card balances, for example, compound interest works against you. Credit card interest rates are typically presented as an annual percentage rate (APR). However, you'll want to consider the annual percentage yield (APY), which takes into account compounding throughout the year to reflect how much your balance increases.

Talk to Commonwealth Credit Union About Your Savings Options

Understanding how compound interest works helps you make smarter financial decisions. To take advantage of compound growth, review the savings account and certificate options that Commonwealth Credit Union offers our members. Visit our website or speak with a local team member to learn more about your savings strategy!.

Image credit: // Shutterstock // mapo_japan